Market Consolidation Trends in China Lingerie Industry News

- 时间:

- 浏览:123

- 来源:CN Lingerie Hub

If you're keeping an eye on the China lingerie industry, one thing’s become crystal clear: we’re in the middle of a major market shake-up. Big brands are getting bigger, small players are scrambling, and consolidation is no longer just a buzzword—it’s the new reality.

I’ve been tracking this space for over five years, and what I’m seeing now isn’t just growth—it’s transformation. The old model of flooding the market with low-cost, mass-produced bras? That ship has sailed. Today, it’s all about quality, branding, and smart digital strategies. And if you're not adapting, you're disappearing.

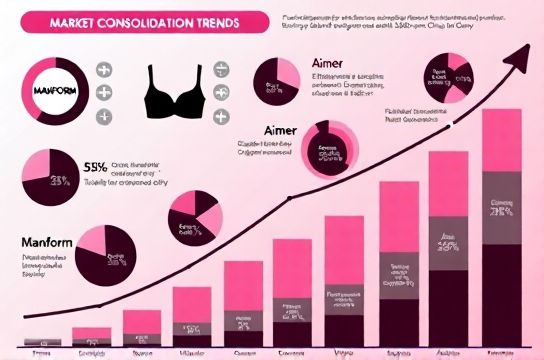

Let’s break it down with some hard numbers. According to Euromonitor, the top 5 brands in China’s lingerie market now control nearly 43% of total revenue—up from 32% just five years ago. That’s massive concentration in a traditionally fragmented market.

Who’s Winning the China Lingerie Race?

The leaders? Brands like Maniform, Triumph China, and Aimer. These aren’t just legacy names—they’ve reinvented themselves with data-driven retail, AI-powered fit recommendations, and serious e-commerce muscle. In fact, Aimer reported a 28% year-on-year increase in online sales in 2023, while physical stores only grew by 6%. That shift tells you everything.

Here’s a snapshot of market share trends:

| Brand | 2019 Market Share (%) | 2023 Market Share (%) | Sales Growth (CAGR) |

|---|---|---|---|

| Maniform | 9.1 | 12.4 | 10.3% |

| Triumph China | 7.8 | 10.1 | 8.7% |

| Aimer | 6.5 | 9.3 | 9.5% |

| Other Local & International | 76.6 | 68.2 | 3.2% |

Notice how the 'Others' category is shrinking fast? That’s consolidation in action. Smaller brands can’t compete with the ad spend, supply chain efficiency, or tech integration of the big players.

Why Is This Happening Now?

Three big drivers:

- Rising consumer expectations: Chinese shoppers now demand comfort, style, and inclusivity. They’re also more informed—thanks to social media and KOL reviews.

- Digital dominance: Over 65% of lingerie purchases in China now happen online or via livestream commerce. The winners are those mastering Douyin, Xiaohongshu, and Tmall.

- Supply chain pressure: Post-pandemic logistics and raw material costs hit small brands hardest. Economies of scale matter more than ever.

So what should brands do? If you're a smaller player, niche down. Think specialized fits, eco-friendly materials, or localized storytelling. Or consider merging—many mid-tier brands are exploring partnerships to survive.

For consumers, this trend means better products but fewer choices. For investors? It’s a golden opportunity to back the consolidators.

Want to understand how this affects your buying decisions? Check out our full guide on China lingerie trends. Or if you're a brand looking to navigate this shift, dive into our strategic playbook on market consolidation strategies.